This Offering includes two strategically selected Small Bay Properties with high occupancy rates in Miami, Florida and Richardson, Texas.

Quick Links

3rd Party Due Diligence Report

Coming Soon

Sign Selling Agreement via DocuSign

Request a Link to Sign Below

Marketing Materials

Offering

Snapshot

This Offering presents a portfolio of two small bay industrial properties located in the Miami-Fort Lauderdale-West Palm Beach metropolitan statistical area (the “Miami MSA”) and Dallas-Fort Worth metropolitan statistical area (the “DFW MSA”). We believe that small bay industrial, or light-industrial, properties offer several advantages including but not limited to a concentrated tenant base with long-term leases, are typically located in more densely-populated infill areas, and benefit from higher barriers to entry and replacement costs. Leases for these properties are generally shorter in term, allowing rents to adjust more quickly in response to market shifts and evolving demand. These leases often include annual contractual rent increases, supporting consistent rent growth throughout the lease term.

Acquisition Details

Total Acquisition Cost1

$86,671,730

Total Capitalization

$91,382,493

Lender Reserves2

$6,467,631

Highlights of the Trust

Offering Size

$50,382,493

Minimum Purchase – Cash

$100,000

Minimum Purchase – 1031

$100,000

Suitability

Accredited Investors Only

Loan Information

Loan Amount

$41,000,000

Loan-to-Capitalization3

44.9%

Interest Rate

5.708% Fixed Rate

Amortization

Interest Only for Full Term

1. Total Acquisition Cost includes the down payment made on each Property, the Loan-Related Costs, the Lender Reserves, certain Trust-controlled reserves, the Facilitation Fee, and the Other Closing Costs. 2. Lender Reserves refers to the Capital Expense Reserve, Tax Reserve, Insurance Reserve, Required Repairs Reserve, and Rollover Reserve. 3. The loan-to-capitalization ratio (“LTC”) is the ratio of a loan to the capitalization of an asset purchased. For instance, if someone borrows $80,000 to purchase a property worth $100,000, the LTC ratio is $80,000 to $100,000 or $80,000/$100,000, or 80%.

Please review the entire PPM prior to investing. This material does not constitute an offer to sell. Reference is made to the PPM for a statement of risks and terms of the Offering. The information set forth herein is qualified in its entirety by the PPM. All potential Purchasers must read the PPM and no person may invest without acknowledging the receipt and complete review of the PPM.

Small Bay Real Estate

An Asset Class for an Underserved Tenant Base

Small bay properties are often referred to as multi-tenant warehousing or light industrial properties, and are typically smaller than standard facilities. Roughly 20% of a small bay property is used as an office, and the other 80% is used as a warehouse. The tenants of small bay properties range from small “mom-and-pop” businesses in local distribution, construction, light industrial, and service industries to Fortune 500 companies whose spaces typically average about 2,500 square feet.

UNDERVALUED

ASSET CLASS

LIMITED

INSTITUTIONAL

COMPETITION

SUPERIOR

LOCATIONS

CONTINUED MARK-TO-MARKET OPPORTUNITIES

Diversified Tenant Base

HIGHLY

FRAGMENTED

HIGH BARRIERS TO ENTRY

STRONG

LEASING

MOMENTUM

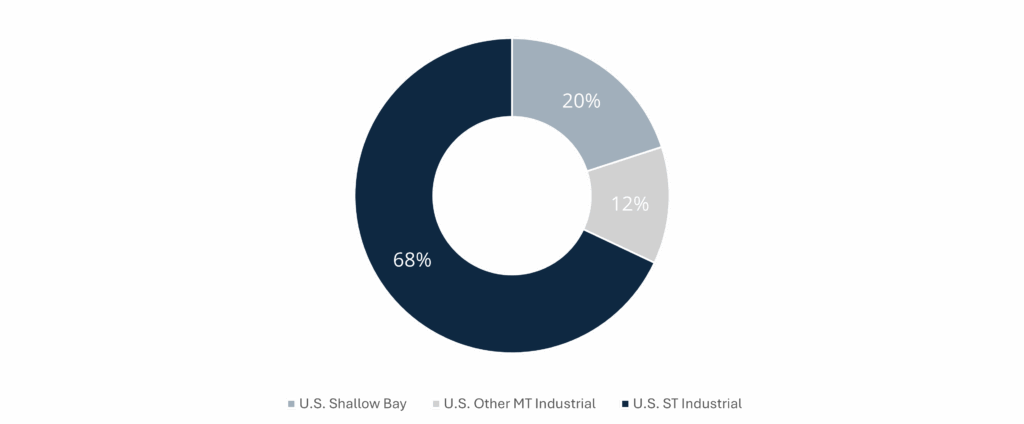

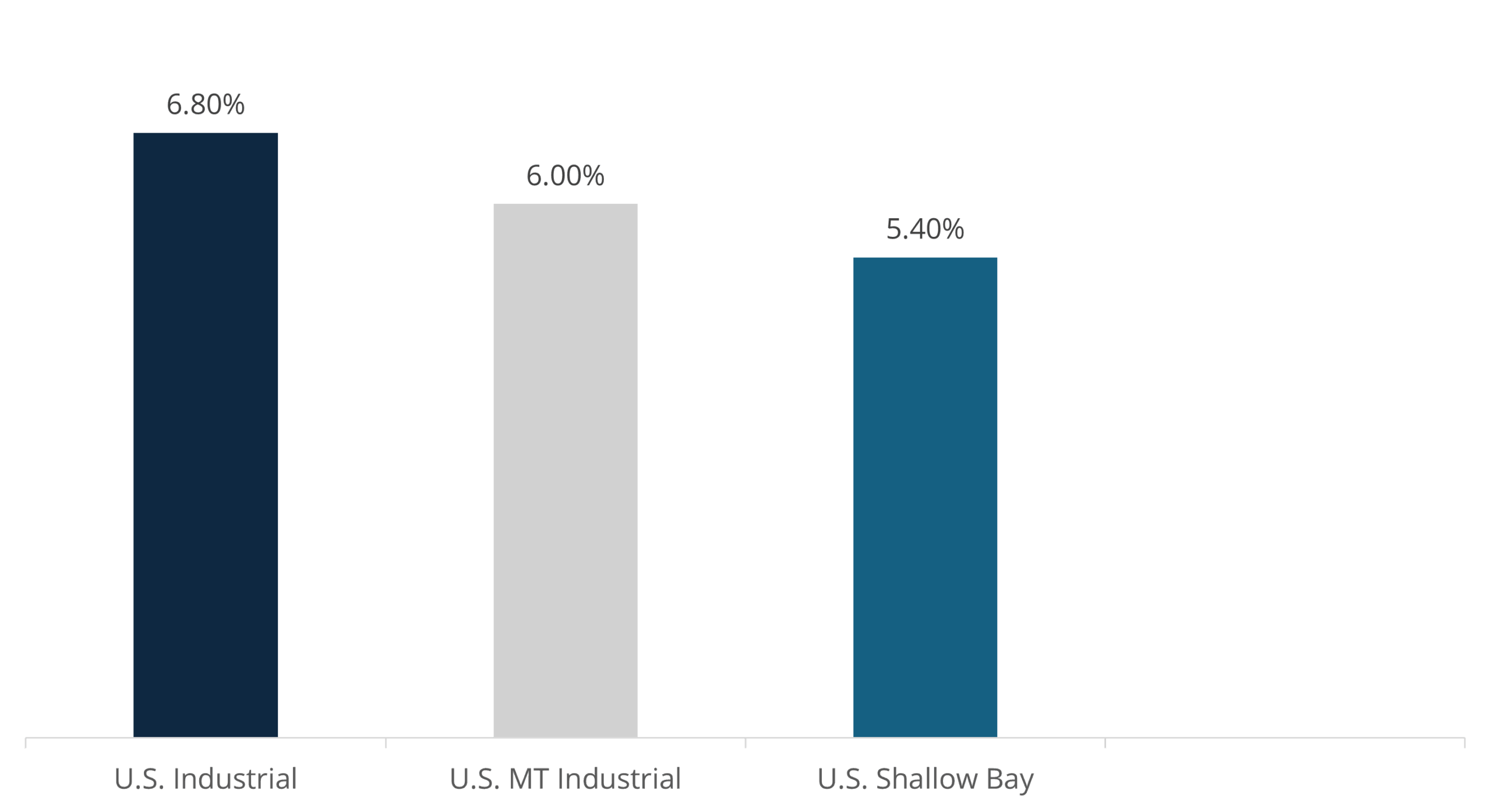

Small Bay Properties account for 20% of the industrial sector space.1 Small Bay is seen as a smaller sub-sector of the industrial sector and has minimal incoming supply compared to typical industrial properties due to high replacement costs. Tight vacancy creates an opportunity for rent growth among tenants, since the demand is higher than the real estate sector supply itself.

2024 Inventory Breakdown1

% Growth in SF Inventory 2012-20241

1. JLL, Shallow Bay Industrial Report, June 2024

Offering Overview

Richardson, Texas

Arapaho Business Park2

Richardson, Texas 75081

The Arapaho Property is located in the DFW MSA, one of the nation’s fastest-growing MSAs. Spanning across roughly 8,675 square miles, the DFW MSA ranks 4th in most populous MSAs and leads Texas in population growth, median household income and job creation.1 As the population grows, demand for commercial real estate – particularly industrial properties – continues to be on the rise. With a diverse and stable employment base, the market is well-positioned for continued growth.

Arapaho Business Park consists of 19 buildings on over 31 acres. The Property consists of 407,669 SF of rentable spaces which, as of July 31, 2025, is over 90% occupied. Arapaho Business Park features clear heights between 12’ and 16’, premium location of Highway 75, and multiple buildings with several points of entry for easy access.

| Clear Heights | 12′-16′ |

| Parking Spaces | 1,552 |

| Years Built | 1976-1980 |

| Total Acres | 31.55 |

| Total Rentable SF | 407,669 |

| AVG. Rent/SQFT2 | $12.73 |

| Occupancy2 | 92.1% |

| Weighted Avg. Lease Term2 | 1.50 YRS] |

1. Esri 2024. Compiled by Partner Valuation Advisors. 2. As of August 31, 2025

Offering Overview

Deerfield Beach, Florida

Deerfield

Deerfield Beach, Florida 33073

The Deerfield property is located in the Miami MSA, a region known for its dynamic economy and diverse population. Covering about 6,137 square miles, the Miami MSA ranks among the top 10 most populous MSAs in the U.S1. Thanks to steady population growth and rising income and education levels, the area’s economy continues to strengthen. As the local economy expands and employment opportunities grow, demand for real estate – particularly Small Bay Properties – is projected to remain strong.

The Deerfield Property offers 97,059 rentable square feet of flex and multi-tenant industrial space across seven buildings. The Property features rear-entry loading with grade-level rollup doors and suite clearance heights between 15’ to 22’. The Deerfield Property is located just 15 miles from downtown Ft. Lauderdale.

| Clear Heights | 15′ – 22′ |

| Parking Spaces | 357 |

| Years Built3 | 1987-1988 |

| Total Acres | 8.25 |

| Total SF | 102,245 SF |

| AVG. Rent/SQFT2 | $15.96/SF |

| Occupancy2 | 95.0% |

| Weighted Avg. Lease Term2 | 2.85 YRS |

1. Esri 2024. Compiled by JLL Valuation Services, LLC. 2. As of August 31, 2025. 3. Two of the buildings were built in 2017, and all of the buildings have gone through significant renovations in 2024-2025.

Basis Industrial

Basis Industrial (“Basis”) is a privately held and vertically integrated real estate owner and operator with over 100 years of combined development, management and acquisition expertise.

Basis focuses on under-managed niche real estate asset classes, including self-storage and multi-tenant industrial warehousing throughout the United States. By focusing on these fragmented asset class verticals that benefit from non-discretionary demand drivers and underrepresented institutional ownership, they can create value through active day-to-day in-house asset management and aggregate economies of scale, leading to potential optimized portfolio and investment performance. Basis is not affiliated with the Sponsor, NexPoint Securities, Inc., or any of their affiliates.

Basis Advantage

Basis’ key principals have over 100 years of combined real estate experience. Basis believes that a robust stable of existing partnerships will create opportunities over the long term to acquire high-quality assets selectively.

Key Growth Drivers:

Property Manager: BaySpace

BaySpace acts as Basis’ in-house Property and Asset Management division. BaySpace utilizes management expertise to improve the current tenant roster. Additionally, BaySpace migrates all tenant communications and interactions to an online platform – including leasing, rental payments, and leasing inquiries. Basis will use its construction and development expertise to improve acquired sites, enhancing the tenant experience and increasing in-place rents on current tenants.

5.3

Million

SQFT of Multi-Tenant Industrial Assets Owned

55

Properties in the Multi-Tenant Industrial portfolio

1.0

Billion

of Total Asset Value in the Multi-Tenant Industrial Portfolio

Property Level Improvements

ACCESS CONTROL & SECURITY

LANDSCAPING, LIGHTING & PAVING

SIGNAGE & VISIBILITY UPDATES

PAINTING & DEFERRED MAINTENANCE

STRIPING & PARKING

Experts in Real Estate

Real Estate Track Record1

$21.9 Billion

In Gross Real Estate Acquisitions2

$956.7MM

Real Estate Transactions in the Last 12 Months2

387

Real Estate Acquisitions2

34

States Invested In

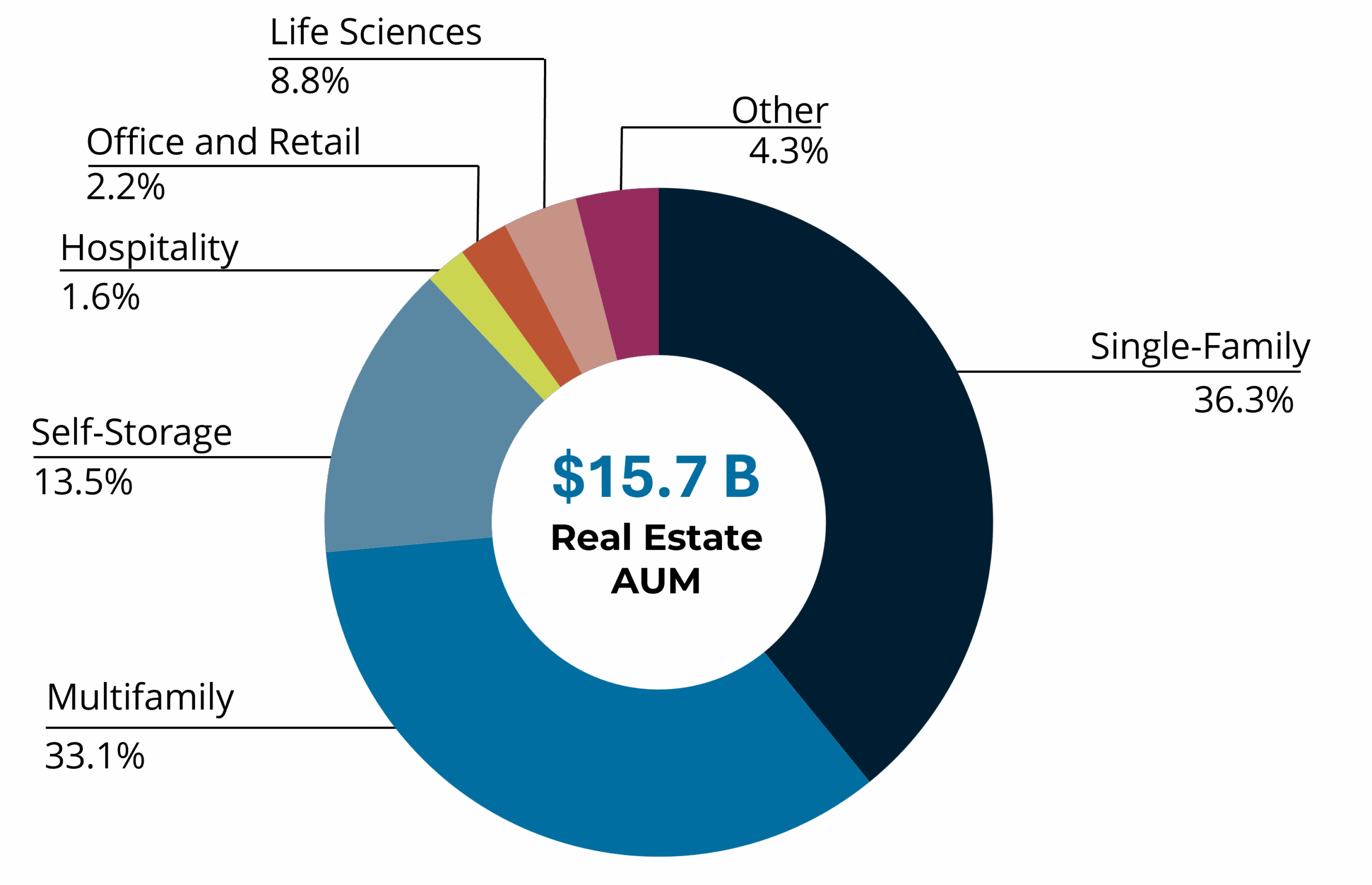

Asset Mix2

1. Real estate assets as of 12/31/2025, inclusive of affiliates. Past performance is not indicative of future results. 2. Real estate assets acquired from January 1, 2012, to December 31, 2025, inclusive of affiliates.

EXPERTS IN REAL ESTATE

Management Team

Matthew McGraner

President

Matthew McGraner is a member of the investment committee for the Sponsor and serves in numerous roles across the NexPoint platform. With over ten years of real estate, private equity, and legal experience, his primary responsibilities are to lead the strategic direction and operations of the real estate platform at NexPoint. McGraner has led the acquisition and financing of approximately $18.4 billion of real estate investments.

Paul Richards

Chief Financial Officer

Paul Richards is Chief Financial Officer at NexPoint Real Estate Advisors, L.P. and serves in numerous roles across the NexPoint platform including leading the financial reporting and accounting teams. He oversees research and conducts due diligence on new investment ideas, performs valuation and benchmark analysis, monitors and manages investments in NexPoint real estate portfolios, and provides industry support to the NexPoint real estate team.

D.C. Sauter

General Counsel

D.C. Sauter is General Counsel for Real Estate for NexPoint Advisors, L.P. Prior to joining NexPoint, he was a partner with Wick Phillips Gould & Martin, LLP, where his practice focused on all aspects of commercial real estate, including acquisitions, dispositions, entitlements, construction, financing, and leasing of industrial, office, retail, hotel, and multifamily assets. In addition to transactional matters, Sauter has significant experience in complex commercial disputes, foreclosures, and workouts.

An investment in NexPoint Small Bay III DST is highly speculative, illiquid and involves substantial risk including the potential loss of your entire investment. The photos presented in this material are of the actual Properties that are part of the Offering. There are substantial risks in any investment program. This is not an offer to sell securities or a solicitation of an offer to buy securities.

An offer to sell interests (“Interests”) in NexPoint Small Bay III DST (the “Parent Trust”) may be made only pursuant to the PPM, which is available upon request. Distributions are not guaranteed. Please review the entire PPM prior to investing. Reference is made to the PPM for a statement of risks and terms of the Offering. The information set forth herein is qualified in its entirety by the PPM. All potential Purchasers must read the PPM and no person may invest without acknowledging receipt and complete review of the PPM. The offering of Interests (the “Offering”) is being made by means of the PPM only to accredited investors who meet minimum accreditation requirements, as well as suitability standards as determined by a qualified broker-dealer or investment advisor. The contents of this communication may not be relied upon in making an investment decision related to this Offering. All prospective Purchasers must read the PPM, including the “Risk Factors” section, any discussion of fees and expenses, and other pertinent information prior to investing. These investment opportunities have not been registered under the Securities Act of 1933 and are being offered pursuant to an exemption therefrom and from applicable state securities laws.

An investment in an Interest is highly speculative and involves substantial risks including, but not limited to:

- this is a “best-efforts” offering with no minimum raise or minimum escrow requirements;

- the lack of liquidity and/or public market for the Interests;

- the holding of a beneficial interest in the Parent Trust with no voting rights with respect to the management or operations of the Trusts or in connection with the sale of the Properties;

- risks associated with owning, financing, operating and leasing Small Bay Properties, and real estate generally, in Florida and Texas, and more specifically the Miami MSA and DFW MSA;

- the Deerfield Property is located in a Hurricane Susceptible Region, which increases the risk of damage to the Deerfield Property;

- risks associated with Small Bay Properties, such as occupancy rate or rent fluctuations, sensitivity to local economic activity and population shifts;

- risks associated with general market fluctuations such as recessions (global or local), the impact of pandemics (including the COVID-19 pandemic), and other systemic market or economic fluctuations of the communities in which the Properties exist;

- the Trusts depend on the Master Tenants for revenue, and the Master Tenants depend on the Tenants for revenue and thus any default by the Master Tenants or the Tenants will adversely affect the Trusts’ operations;

- performance of the Master Tenants under their respective Master Leases, including the potential for the Master Tenants to defer a portion of rent payable under such Master Leases;

- reliance on the Master Tenants and the Property Manager engaged by the Master Tenants, to manage each of the Properties;

- risks associated with Holdings funding the Demand Notes that capitalize each of the Master Tenants;

- risks relating to the terms of the financing for the Properties, including the use of leverage;

- the existence of various conflicts of interest among the Sponsor, the Trusts, the Master Tenants, the Asset Managers, the Property Manager, and their affiliates;

- material tax risks, including treatment of the Interests for purposes of Code Section 1031 and the use of exchange funds to pay acquisition costs, which may result in taxable boot;

- the lack of a public market for the Interests;

- the Interests not being registered with the SEC or any state securities commissions;

- risks relating to the costs of compliance with laws, rules and regulations applicable to the Properties;

- lack of diversity of investment;

- risks related to competition from properties similar to and near the Properties; and

- the possibility of environmental risks related to the Properties.

NexPoint Securities, Inc., an entity under common control with the Sponsor, serves as the Managing Broker-Dealer of the Offering. The Managing Broker-Dealer was formed in November 2013 and is registered as a broker-dealer with the SEC and is a member of FINRA/SIPC.