NexPoint Small Bay I DST

This Offering includes four strategically selected small bay properties with high occupancy rates in two high-growth metropolitan statistical areas (“MSAs”).

3rd Party Due Diligence Report

Sign Selling Agreement via DocuSign

Request a Link to Sign Below

Marketing Materials

Offering Snapshot

This Offering features a portfolio of four small bay properties located in Tampa and Orlando, Florida. NexPoint believes that small bay properties have an advantage over traditional warehouses or industrial facilities, which generally have a concentrated tenant base with long-term leases. Small bay properties tend to be located in more densely-populated infill areas and benefit from higher barriers to entry and replacement costs, and tenant leases of small bay properties are generally for a shorter term, which allows rents to adjust more quickly to market and new demand conditions.

Acquisition Details

| Total Acquisition Cost1 | $96,182,023 |

| Lender Reserves2 | $5,069,465 |

| Total Capitalization | $101,745,817 |

Highlights of the Trust

| Offering Size | $59,505,817 |

| Minimum Purchase -Cash | $100,000 |

| Minimum Purchase -1031 | $100,000 |

| Suitability | Accredited Investor Only |

Loan Information

| Total Loan Amount | $42,240,000 |

| Loan-To-Capitalization | 41.5% |

| Interest Rate | 6.21% Fixed Rate |

| Amortization | Interest Only for Full Term |

11. The Total Acquisition Cost includes the purchase price of the Properties and Other Closing Costs. 2. Lender Reserves refers to the Rollover Reserve, the Replacement Reserve, the Required Repairs Reserve, the Rent Concession Reserve, the Imposition Reserve, and the Unfunded Obligation Reserve. 3. The loan-to-capitalization ratio (“LTC”) is the ratio of a loan to the capitalization of an asset purchased. For instance, if someone borrows $80,000 to purchase a property worth $100,000, the LTC ratio is $80,000 to 100,000 or $80,000/100,00, or 80%.

There are substantial risks in any investment program. See ‘‘ Risk Factors” on page 23 of the PPM for a discussion of the risks relevant to the Offering.

Please review the entire PPM prior to investing. This material does not constitute an offer to sell. Reference is made to the PPM for a statement of risks and terms of the Offering. The information set forth herein is qualified in its entirety by the PPM. All potential Purchasers must read the PPM and no person may invest without acknowledging the receipt and complete review of the PPM.

President's Plaza

Small Bay Real Estate

An Asset Class for an Underserved Tenant Base

Small bay properties are often referred to as multi-tenant warehousing or light industrial properties, and are typically smaller than standard facilities. Roughly 20% of a small bay property is used as an office, and the other 80% is used as a warehouse. The tenants of small bay properties range from small “mom-and-pop” businesses in local distribution, construction, light industrial, and service industries to Fortune 500 companies whose spaces typically average about 2,500 square feet.

UNDERVALUED

ASSET CLASS

LIMITED

INSTITUTIONAL

COMPETITION

SUPERIOR

LOCATIONS

CONTINUED MARK-TO-MARKET OPPORTUNITIES

FLEXIBLE LEASE TERMS / MARKET RENTAL RATE

HIGHLY

FRAGMENTED

MINIMAL

FUTURE

CAPITAL COSTS

DEDICATED

MANAGEMENT

TEAM

POTENTIAL

CASH FLOWS

HIGH BARRIERS TO ENTRY

RISE OF

E-COMMERCE

STRONG

LEASING

MOMENTUM

Small bay warehouses and industrial facilities are a significant property sector, accounting for over one-quarter of all competitive, investable industrial space. This asset class, however, we believe undervalued by institutional investors.

Broad Tenant Mix

In general, small bay facilities are multi-tenanted and serve a board mix of tenants in local distribution, construction, light industrial and service industries. The facilities often have ground level doors, and lower clearance heights than larger distribution facilities.

Limited Institutional Capital

Institutional investors are underweight in this industrial market segment, as small bay warehouse facilities account for only 9.7% of institutional industrial investments1. Small bay properties are more likely to be held by local or regional private owners and developers, hence ownership tends to be highly fragmented. This presents opportunities in creating economies of scale in property acquisitions and management for larger integrated investment platforms.

Significant Portion of Real Estate

Small bay warehouse facilities are a significant property sector, accounting for over one quarter of all competitive, investable industrial space1.

1.CBRE: The case for Small Bay warehouse

The Corporex Property, President’s Property, and Brandywine Property are located in the Tampa MSA, 2,515 square miles in size. The Tampa MSA’s economy is expected to benefit from a growing population base and higher education levels. The Tampa MSA saw an increase in the number of jobs in the past ten years, has maintained a lower unemployment rate than the State of Florida, and has a higher GDP per capita than the State of Florida.

3.25

Current Population1

1.3

Annual Population Growth (from 2010-2022) 1

94,566

Avg. Household Income1

2.2

Unemployment Rate1

9.6%

5-YR Employment Growth1

3

Most Popular City to Move To3

*JLL Valuation & Advisory Services, LLC

The Tampa MSA region serves as the “gateway” to Florida’s High-Tech Corridor, a regional economic development initiative between the University of Central Florida, the University of South Florida, and the University of Florida to grow the technology sector through partnerships supporting research, marketing, workforce, and entrepreneurship.

Properties

Presidents Plaza1

4801 GEORGE ROAD, TAMPA, FL 33634

Presidents Plaza offers garden-style office suites with large glass paned windows and provides an abundant amount of natural lighting. Rear entry loading with grade-level rollup doors and suite clear heights of 15’. The Property is minutes from Hillsborough Ave, the Veteran’s Expressway, the Tampa International Airport, and I-275.

| Loading Doors | 17 |

| Parking Spaces | 12 |

| Year Built | 1988 |

| Total Acres | 4.04 |

| Total Square Feet | 44,583 |

| Avg. Rent/SqFT | $10.01 |

| Occupancy | 92.3% |

| Avg. Lease Term | 1.86 Yrs |

1. As of 6/26/23

Corporex5

3904 CORPOREX DRIVE, TAMPA, FL 33619

Corporex Plaza offers garden-style office suites with large glass paned windows and abundant natural lighting. Rear loading options include dock-high and grade-level doors, with suite clearance heights ranging from 14’ to 18’. The Property is well situated with easy access to I-4, I-75, US 41, US 301 & the Selmon Expressway.

| Loading Doors | 31 |

| Parking Spaces | 199 |

| Years Built | 1984-85 |

| Total Acres | 6.55 |

| Total Square Feet | 100,265 |

| Avg. Rent/SqFT | $9.16 |

| Occupancy | 87.4% |

| Avg. Lease Term | 1.19 YRS |

Brandywine5

3801 CORPOREX DRIVE, TAMPA, FL 33619

The Brandywine Business Center offers flexible office and warehouse configurations with large glass-paned storefronts. Most suites have either rear van, dock-high loading doors, or grade level service doors. The Property is conveniently located near Dr. MLK Jr. Blvd and I-4 and is 15 minutes from the Tampa International Airport.

| Loading Doors | 34 |

| Parking Spaces | 176 |

| Year Built | 1986 |

| Total Acres | 5.54 |

| Total Square Feet | 79,124 |

| Avg. Rent/SqFT | $11.24 |

| Occupancy | 100.0% |

| Avg. Lease Term | 2.42 Yrs |

1. JLL Valuation & Advisory Services, LLC 2. CBRE Research/US Census Data, May 2023 3. US Bureau of Labor Statistics, CBRE Research,

May 2023 4. RedFin; April 2023 – June 2023 5. As of 6/26/23.

Offering Overview

Orlando, FL

The Orlando Property is located in the Orlando MSA. The Orlando MSA is 3,491 square miles in size and ranks twenty-second in population out of the nation’s 382 MSAs1. The Orlando MSA’s economy is expected to benefit from a growing population base and higher income and education levels. The Orlando MSA saw an increase in the number of jobs in the past ten years, and its employment growth is expected to continue. Additionally, the Orlando MSA has had a higher GDP growth rate in the past nine years and a higher GDP per capita than the State of Florida overall.

2,799,598

2022 Population2

2.3%

Annual Population Growth Since 20202

67,299

Avg. Household Income2

2.6

Unemployment Rate3

30.9

Increase in Employment Growth since 20133

2

in the Country for job Growth3

MAJOR EMPLOYERS

Walt Disney World Resort, Advent Health, Orange County Public Schools, Universal Orlando Resort, Orlando Health, Publix, University of Central Florida, Seminole County Public Schools, and Lockheed Martin

Source: JLL Valuation

1. JLL Valuation & Advisory Services, LLC 2. Esri 2023, Complied by JLL

Valuation & Advisory Services, LLC 3. Bureau of Labor Statistics

Orlando Business Plaza1

The Orlando International Business Center is a six building, ~195,000 square foot small bay property located less than four miles from the Orlando International Airport. The office park lends itself to flexibility due to the number of buildings and spaces, and offers warehouse space with grade-level doors.

31

Loading Doors

520

Parking Spaces

520

Parking Spaces

1983-87

Years Built

2020-22

Years Renovated

196,268

Total SQFT

12.87

Avg. Rent/SQFT

93.6

Occupancy

2.60

Avg. Lease Term

Featured Tenants

1As of 6/26/23

Basis Industrial

Basis Industrial (“Basis”) is a privately held and vertically integrated real estate owner and operator with over 100 years of combined development, management and acquisition expertise.

Basis focuses on under-managed niche real estate asset classes, including self-storage and multi-tenant industrial warehousing throughout the United States. By focusing on these fragmented asset class verticals that benefit from non-discretionary demand drivers and underrepresented institutional ownership, They can create value through active day-to-day in-house asset management and aggregate economies of scale, leading to potential optimized portfolio and investment performance.

Basis Advantage

Basis’ key principals have over 100 years of combined real estate experience. Basis believes that a robust stable of existing partnerships will create opportunities over the long term to acquire high-quality assets selectively.

Key Growth Drivers:

Property Manager: BaySpace

BaySpace acts as Basis in-house Property and Asset Management division. BaySpace utilizes management expertise to improve the current tenant roster. Additionally, BaySpace migrates all tenant communications and interactions to an online platform – including leasing, rental payments, and leasing inquiries.

Basis will use its construction and development expertise to improve acquired sites, enhancing the tenant experience and increasing in-place rents on current tenants.

1.3

Million SQFT of Multi-Tenant Industrial Assets Owned

24

Properties in the Multi-Tenant Industrial portfolio

325

Million of Total Asset Value in the Multi-Tenant Industrial Portfolio

Property Level Improvements

ACCESS CONTROL & SECURITY

LANDSCAPING, LIGHTING & PAVING

SIGNAGE & VISIBILITY UPDATES

PAINTING & DEFERRED MAINTENANCE

STRIPING & PARKING

Experts in Real Estate

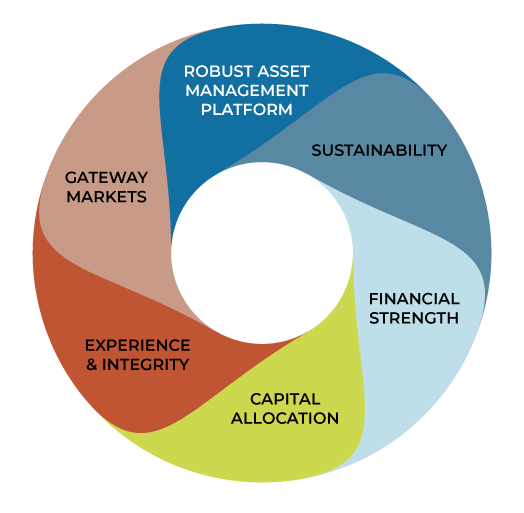

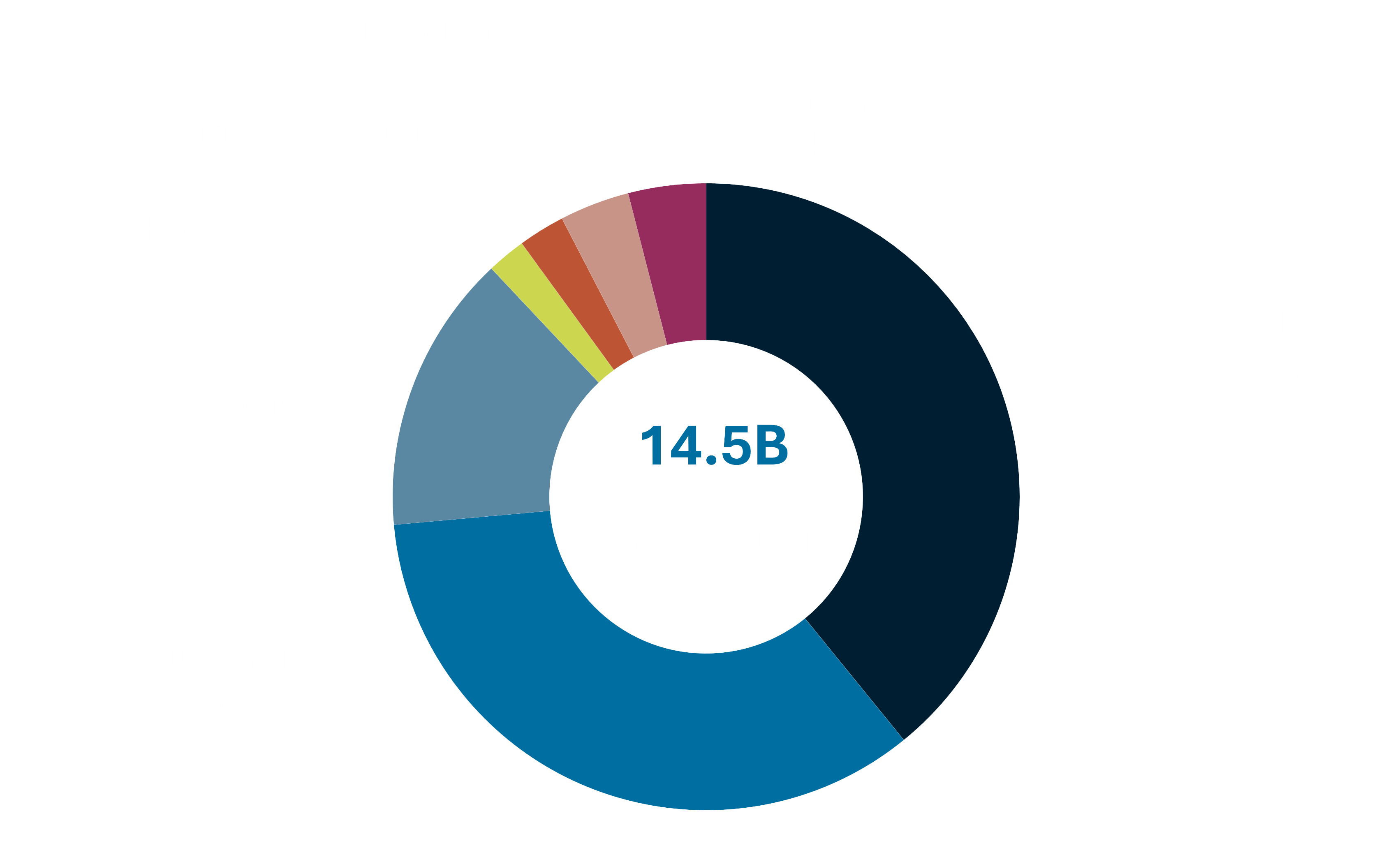

Real Estate Track Record1

$20.1 Billion

In Gross Real Estate Acquisitions2

$534.5 Million

Real Estate Transactions in the Last 12 Months2

357

Real Estate Acquisitions2

34

States Invested In

Asset Mix2

1. Real estate assets as of 09/30/2024, inclusive of affiliates. 2. Real estate assets acquired from January 1, 2012 to September 30, 2024, inclusive of affiliates.

EXPERTS IN REAL ESTATE

Management Team

Matthew McGraner

President

Matthew McGraner is a member of the investment committee for the Sponsor and serves in numerous roles across the NexPoint platform. With over ten years of real estate, private equity, and legal experience, his primary responsibilities are to lead the strategic direction and operations of the real estate platform at NexPoint. McGraner has led the acquisition and financing of approximately $18.4 billion of real estate investments.

Brian Mitts

Chief Financial Officer

Brian Mitts is a member of the investment committee for the Sponsor and serves in numerous roles across the NexPoint platform. Currently, Mitts leads NexPoint’s financial reporting and accounting teams and is integral in financing and capital allocation decisions. Mitts was also a co-founder of NREA, as well as NXRT and NexPoint Advisors, L.P., the parent of NREA. He has worked for NREA or one of its affiliates since 2007.

D.C. Sauter

General Counsel

D.C. Sauter is General Counsel for Real Estate for NexPoint Advisors, L.P. Prior to joining NexPoint, he was a partner with Wick Phillips Gould & Martin, LLP, where his practice focused on all aspects of commercial real estate, including acquisitions, dispositions, entitlements, construction, financing, and leasing of industrial, office, retail, hotel, and multifamily assets. In addition to transactional matters, Sauter has significant experience in complex commercial disputes, foreclosures, and workouts.

An investment in NexPoint Small Bay I DST is highly speculative, illiquid and involves substantial risk including the potential loss of your entire investment. The photos presented in this brochure are of the actual Properties that are part of the Offering.

There are substantial risks in any investment program. See “Risk Factors” on page 23 of the accompanying PPM for a discussion of the risks relevant to this Offering. Distributions are not guaranteed. Please review the entire PPM prior to investing. Reference is made to the PPM for a statement of risks and terms of the Offering. The information set forth herein is qualified in its entirety by the PPM. All prospective Purchasers must read the PPM and no person may invest without acknowledging receipt and complete review of the PPM.

An investment in an Interest is highly speculative and involves substantial risks including, but not limited to:

- this is a “best-efforts” offering with no minimum raise or minimum escrow requirements;

- the lack of liquidity and/or public market for the Interests;

- the holding of a beneficial interest in the Parent Trust with no voting rights with respect to the management or operations of the Trusts or in connection with the sale of the Properties;

- risks associated with owning, financing, operating and leasing small bay properties, and real estate generally, in Florida, and more specifically the Tampa – St. Petersburg – Clearwater Metropolitan Statistical Area (the “Tampa MSA”) and the Orlando – Kissimmee – Sanford Metropolitan Statistical Area (the “Orlando MSA”);

- the Properties are located in a “Hurricane Susceptible Region,” which increases the risk of damage to the Properties;

- risks associated with small bay properties, such as occupancy rate or rent fluctuations, sensitivity to local economic activity and population shifts;

- risks associated with general market fluctuations such as recessions (global or local), the impact of pandemics (including the COVID-19 pandemic), and other systemic market or economic fluctuations of the communities in which the Properties exist;

- the Trusts depend on the Master Tenants for revenue, and the Master Tenants depend on the Tenants for revenue and thus any default by the Master Tenants or the Tenants will adversely affect the Trusts’ operations;

- performance of the Master Tenants under their respective Master Leases, including the potential

- for the Master Tenants to defer a portion of rent payable under such Master Leases;

- reliance on the Master Tenants and the Property Manager engaged by the Master Tenants, to manage each of the Properties;

- risks associated with the Sponsor funding the Demand Notes (as defined herein) that capitalize each of the Master Tenants;

- risks relating to the terms of the financing for the Properties, including the use of leverage;

- the existence of various conflicts of interest among the Sponsor, the Trusts, the Master Tenants, the Asset Manager, the Property Manager, and their affiliates;

- material tax risks, including treatment of the Interests for purposes of Code Section 1031 and the use of exchange funds to pay acquisition costs, which may result in taxable boot;

- the lack of a public market for the Interests;

- the Interests not being registered with the Securities and Exchange Commission (the “SEC”) or any state securities commissions;

- risks relating to the costs of compliance with laws, rules and regulations applicable to the Properties;

- lack of diversity of investment;

- risks related to competition from properties similar to and near the Properties; and

- the possibility of environmental risks related to the Properties.

NexPoint Securities, Inc., an entity under common control with the Sponsor, serves as the Managing Broker-Dealer of the Offering. The Managing Broker-Dealer was formed in November 2013 and is registered as a broker-dealer with the SEC and is a member of FINRA/SIPC.

PLEASE CONTACT YOUR ADVISOR WITH ANY QUESTIONS ABOUT THIS OFFERING.